Where did ISA come form?

Learn how we are translating other forms of financing to promote dignity in our UPG approach

Dr Solomon Wambua

8/30/20252 min read

What Is an Income Sharing Agreement (ISA)?

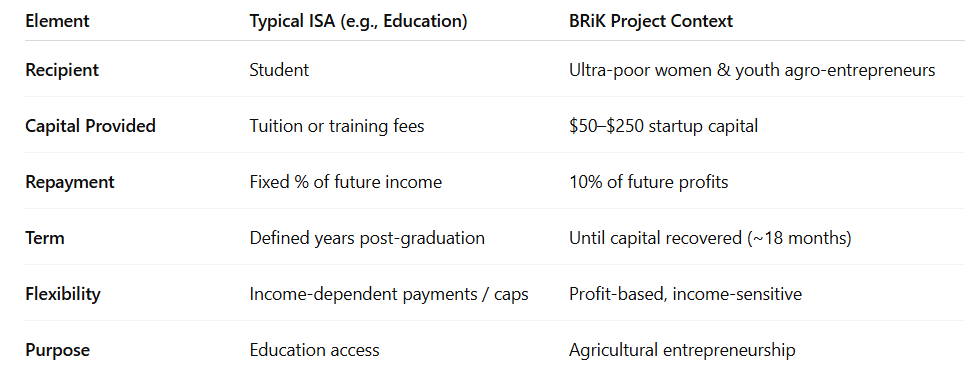

An Income Sharing Agreement (ISA) is a financial tool where an investor or organization provides upfront capital to someone—traditionally a student or trainee—and the recipient agrees to pay back a fixed percentage of future earnings over a set period of time or until a certain amount is repaid. Unlike traditional loans, ISAs typically don’t charge interest and repayments are tied directly to income levels, offering built-in flexibility and risk-sharing.

ISAs were first proposed by economist Milton Friedman in 1955, suggesting they function like equity in a person—funding them upfront and sharing future income returns.

How ISAs Work in Practice (Education Case)

In education, ISAs have been used to fund tuition for students who then pay, for example, 5% of their monthly income for 8–10 years post-graduation. Organizations like Chancen International in East Africa have adapted this model to support students by offering interest-free financial support in exchange for a portion of future income—enabling equitable access to education without collateral.

Applying ISA in the BRiK Project (Agriculture-Focused Context)

In your BRiK pilot, this model is tailored to agriculture entrepreneurship:

Capital Injection

Each participant (30 ultra-poor women and youth) receives $50–$250 to start their agro-enterprise.

Shared Risk, Shared Dignity

Participants pledge to repay 10% of their future profits over a defined period (e.g., until the transfer is recovered, up to 18 months). This approach aligns incentives: both parties benefit as the business succeeds.

Why It Matters

Unlike traditional loans that can be burdensome, this ISA model:

Requires no collateral.

Scales with income—repayments are manageable when earnings are higher.

Keeps capital revolving—once repaid, it funds the next participant.

Parallel Benefits

Empowers beneficiaries to build profitable agro-enterprises.

Encourages accountability and financial discipline.

Promotes sustainable scaling as the fund continually replenishes with each repayment cycle.

Real-World Precedents

Chancen International—East Africa’s largest ISA provider—serves thousands of students and reports that beneficiaries earn up to four times the national median income upon repayment.

One Acre Fund, a major agricultural nonprofit in East Africa, reports that farmers using its asset-based financing and training model achieved 33% higher profits compared to non-participants. While not strictly an ISA, it demonstrates how tailored support can produce strong financial results in agro settings.

An ISA in the BRiK Project transforms capital intervention into a shared, dignified pathway to sustainable income. Participants receive essential seed funding and repay only when they earn from their agro-enterprise. It balances empowerment with accountability, and—if successful—creates a model that can be replicated across communities, fueling long-term impact and resilience.

Summary Table: Standard ISA vs. BRiK Agricultural ISA